🏴☠️ ⚡️ Achieving the ARR Productivity of a $50M+ SaaS Firm (Operating Concept)

We are Acquiring and Operating Micro SaaS firms in public. Join us every Saturday morning for acquisition strategies and deal analysis, value creation playbooks, operating concepts and more...

Welcome back!

In case you missed it, we are ACTIVELY pursuing our 2nd acquisition. If you are exploring an exit or have someone in your world who might be, I am 100% available to discuss performance metrics and opportunites to enhance valuation (so the convo is productive no matter the outcome).

Here’s the quick / dirty version of what we look for:

// Sector: Niche Vertical B2B SaaS — catered to a defined industry that represents less than 250k US Business Entities and is stable (20% or less growth) with a high presence of SMBs and fragmented competition

// ARR: $500k to $1.5M

// User Retention (MoM): >96%

// Profit Margin: >25%

// Onboarding: User-led

// Founder / Team: Technical

Easiest to reply to this email, and we’ll go from there!

Now, on with the show…

TABLE OF CONTENTS:

RETURN ON EFFORT AS A GUIDING PRINCIPLE IN BUSINESS

MEASURING PRODUCTIVITY

RETURN ON EFFORT = OPERATING LEVERAGE

RETURN ON EFFORT IN MICRO SAAS

📺 WATCH:

📻 LISTEN:

RETURN ON EFFORT AS A GUIDING PRINCIPLE IN GAME SELECTION

Conventional wisdom in acquisition entrepreneurship, lower middle market buyouts, etc., is to do the biggest deals possible.

If you want to fly to the moon, you might as well fly to Mars. Both have a similar degree of difficulty, and Mars is much cooler.

It’s hard to generate amazing outcomes (or the almighty alpha) when all players pursue the same deals or strategy.

The point of business is to generate as much profit as possible from every dollar of revenue and defend this position over time (where theory dictates that all profits are eventually competed away). Pursuing larger deals makes sense only if they support this result.

I’m here to suggest they don’t.

I’ve been studying the macro concept of ‘return on effort’ to communicate the potential of Micro SaaS and help rationalize our intention to avoid the biggest deals (when the default perception is big = better return on effort, or otherwise).

By the end of this, hopefully you agree with me.

However, you’ll quickly move to the next most interesting question: How do you repeat an individual Micro SaaS firm’s productivity to achieve meaningful scale? Think: A 70% profit margin on a $500k revenue business is interesting, but that’s still only a $350k profit. It's tough to change lives with that unless you can stack multiple units without a comparable increase in operational burden and complexity…

I’ll save that for another time. Let’s move on to exploring return on effort as a core driver of game selection…

MEASURING PRODUCTIVITY

Let’s start with some high-level, org-wide metrics that have endured the test of time.

CAC Ratio

What it means: How well a firm converts sales and marketing spend into new revenue. The lower, the better.

How to calculate: Total Sales & Marketing Spend/Net New Revenue

Burn Ratio

What it means: How well a firm converts total cash spend (across the whole business) into new revenue. It is most commonly used to determine a firm’s runway (cash to feed operations before they die or need to raise capital). The lower, the better.

How to calculate: Total net cash burn/ Net New Revenue

The above metrics abstract beyond individual contributors to look at the effectiveness of the overarching machine, mainly as it relates to converting capital into growth.

If we zoom in on contributor-level metrics, there are two most common in SaaS:

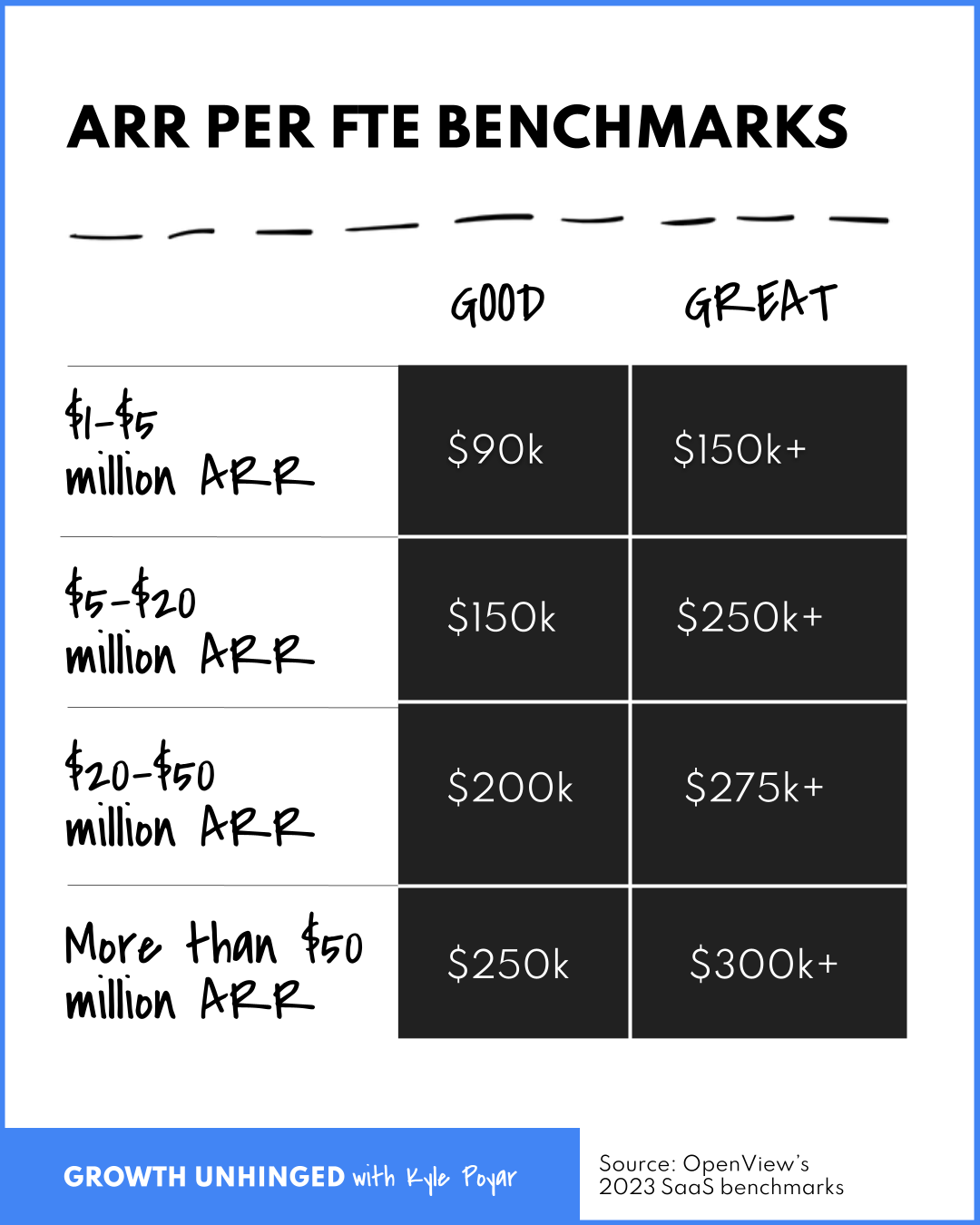

ARR / FTE

What it means: How well a company leverages human capital to generate annual recurring revenue

How to measure: Annual Recurring Revenue/Total Full-time Equivalents (aka employees or anyone working 174hrs per month)

This is what good and great look like in Private SaaS at different ARR thresholds (full article is worth the read). Spoiler: ARR / FTE grows with scale…

EBITDA / FTE

ARR / FTE is a VERY prominent metric in the VC game for reasons discussed last week. With the zero interest rate glory days behind us, the convention is shifting hard and fast to EBITDA / FTE as a truer proxy for investors to latch on to after they interpret a firm’s general position in the landscape via ARR / FTE (team size, number of customers and products, etc.).

(To dive deeper into this, I highly recommend: Are Revenue Multiples a Thing of the Past?)

What it means: How well a company leverages human capital to generate profit

How to measure: EBITDA (or Operating Profi)/Total Full-time Equivalents (aka employees or anyone working 174hrs per month)

EBITDA / FTE is, without question, the priority in Micro SaaS. As is the Rule of 40 (Growth + Profitability = 40%+).

So, back to the question we started with: do bigger deals indeed provide a greater return on effort, such that we should pursue them?

RETURN ON EFFORT = OPERATING LEVERAGE

Operating leverage is really a function of two things:

How much impact (Revenue or profitability) do you get from fixed costs (personnel, tooling, etc.)?

How much do variable costs scale with revenue (eating at the profit the additional revenue could provide)

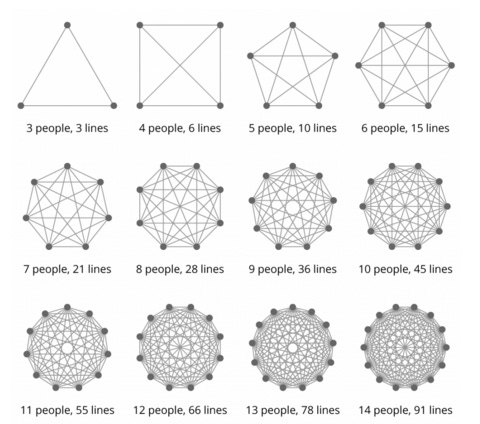

I’m obviously obsessed with operating leverage. I am fascinated with doing more with less. Especially when less translates to fewer humans, as each human has an exponential effect on communication paths (see below), management load, etc.

RETURN ON EFFORT IN MICRO SAAS

So, does Micro SaaS provide a context where high-leverage operating models can exist and thrive, yielding extraordinary return on effort?

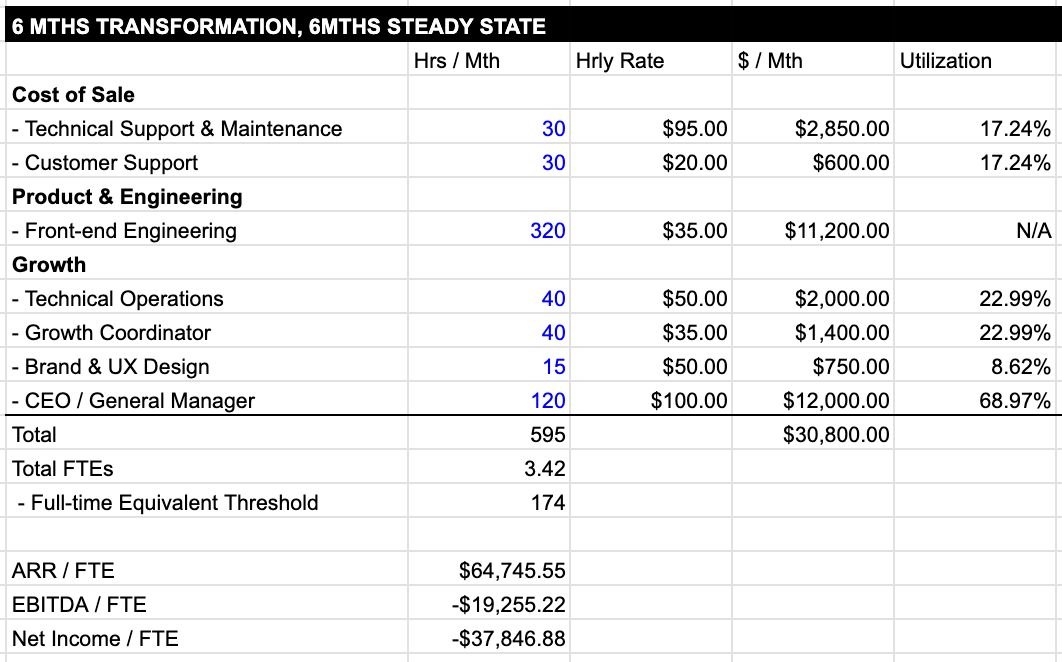

This is the ARR / FTE and EBITDA / FTE profile at our portfolio company during ‘transformation’:

This is the ARR / FTE and EBITDA / FTE profile during ‘steady-state’, after 30% growth:

If you refer back to Openview’s benchmarks above, you’ll notice our port co generates more ARR / FTE than a >$50M ARR Private SaaS firm. More importantly, it generates as much profit productivity (EBITDA / FTE) as a $5-$20M firm yields in revenue productivity (ARR / FTE).

All to say, this suggests extraordinary return on effort.

Now, how do we repeat this EBITDA / FTE profile across a large portfolio…?

For the love of the game. 🏴☠️⚡️

That’s a wrap!

Hit REPLY and let me know what you found most useful this week (or rock the one-question survey below) — truly eager to hear from you…

And please forward this email to whoever might benefit (or use the link below) 🏴☠️ ⚡️